There is now growing concern that in a relatively short time we may be looking down the barrel of an inflationary depression. As anyone who has read my theory knows, this is merely an extreme example of an illusory core paradox in which both horns of the stagflation dilemma --unemployment and inflation-- grow wildly out of hand at the same time. The pundits of the day currently believe that this is an unavoidable feature of economics per se. This is sustained to a large degree by the universal misperception that modern economics is based on money, when in fact, this is not the true foundation at all.

From a superficial perspective, energy is just another increasingly expensive product among a wide range of other, equally important products, and just happens to play a widespread central role. Consequently, everything done by the authorities in order to manipulate and prop up the money system merely serves to exacerbate the prevailing state of decline. Every conventional remedy simply maintains the same vicious circle of reason that produced the problem of decline in the first place.

We can therefore rest assured that a hyper-inflationary scenario, similar to that of the infamous Wiemar Republic, is now in the making. While this possibility is widely believed to be no longer possible, that was before the U.S. began to secretly export its inflation (that is, its excessive printing of currency) overseas with the strategy of "globalization." Unfortunately, there is now simply no place left to export the economic incompetence of the U.S. government and chickens are coming home to roost.

From a superficial perspective, energy is just another increasingly expensive product among a wide range of other, equally important products, and just happens to play a widespread central role. Consequently, everything done by the authorities in order to manipulate and prop up the money system merely serves to exacerbate the prevailing state of decline. Every conventional remedy simply maintains the same vicious circle of reason that produced the problem of decline in the first place.

We can therefore rest assured that a hyper-inflationary scenario, similar to that of the infamous Wiemar Republic, is now in the making. While this possibility is widely believed to be no longer possible, that was before the U.S. began to secretly export its inflation (that is, its excessive printing of currency) overseas with the strategy of "globalization." Unfortunately, there is now simply no place left to export the economic incompetence of the U.S. government and chickens are coming home to roost.

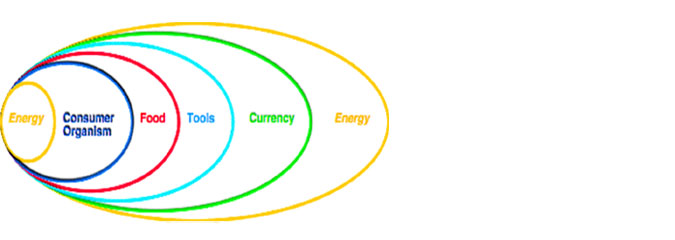

As I've said repeatedly, and will continue to restate in as many ways as I can think of, the only way up and out of this mess without a full scale collapse is to collectively grasp in what way any and every given economic system is nothing more nor less than an energy system in the purest and most fundamental sense, and not just an arbitrary process of multiple components and loosely associated factors held together by an abstract system of currency. Energy is the fundamental essence behind the entire spectrum of goods and services that comprise any given economic system. Thus in order to produce a truly stable and prosperous system of economics, it is absolutely necessary to fully integrate the value of currency with the only, underlying reality; thus my advocacy for a 'Joule Standard.'

But the adoption of a Joule Standard has multifaceted consequences. It's adoption implies more than merely equating the denominations of a currency with some arbitrary quantity of energy. It also implies the adoption of an altogether different function and role of government itself, while simultaneously expunging the concept of taxation altogether from the equation of its existence. In brief, one of the first practical steps towards resolving the paradox of economic decline is to systematically replace the practice of taxation with the production of energy as a governmental service to society at large. In this manner, governmental services may be funded without the government becoming an ever-expanding, parasitical burden on the very population it was intended to serve.

Everyone today actually believes that taxes are as inevitable as death, when in reality, it's merely an artifact of muddled economic concepts. Every vestige of taxation can be entirely removed from the phenomenon of government, and the cost of government from the cost of every product; unlike today, in which the cost of taxes accumulate to an extraordinary degree before any stage of final consumption. The only way to literally energize an economy is to implement a two-fold approach that addresses (1) the cost of raw energy in every form in terms of energy, and (2) increases the quantities available. The goal is of course, to flood the system with energy.

But the adoption of a Joule Standard has multifaceted consequences. It's adoption implies more than merely equating the denominations of a currency with some arbitrary quantity of energy. It also implies the adoption of an altogether different function and role of government itself, while simultaneously expunging the concept of taxation altogether from the equation of its existence. In brief, one of the first practical steps towards resolving the paradox of economic decline is to systematically replace the practice of taxation with the production of energy as a governmental service to society at large. In this manner, governmental services may be funded without the government becoming an ever-expanding, parasitical burden on the very population it was intended to serve.

Everyone today actually believes that taxes are as inevitable as death, when in reality, it's merely an artifact of muddled economic concepts. Every vestige of taxation can be entirely removed from the phenomenon of government, and the cost of government from the cost of every product; unlike today, in which the cost of taxes accumulate to an extraordinary degree before any stage of final consumption. The only way to literally energize an economy is to implement a two-fold approach that addresses (1) the cost of raw energy in every form in terms of energy, and (2) increases the quantities available. The goal is of course, to flood the system with energy.